Recognizing Crisis – In The Housing Market

A SAFE INDICATION OF AN APPROACHING CRISIS is the increase of capital and housing construction in gross domestic product. How close to collapsing is the Russian market? The real estate crisis in Athens 2300 shares the same causalities as modern crisis – focusing of finances in the hands of bankers (churches back in the day), corruption loan distribution and economic tendency towards the capital construction; little has changed since then. Real estate is a unique product. The main means for it is the geographical differentiation, it cannot be substituted with neither import nor export.

Given the combination of lengthy production and ongoing further expenses results in real estate being a commodity of variable demand therefore it’s necessary to provoke crisis of overproduction or deficit for the market. An average manufacturer would be unable to operate in such high risk market if it weren’t for three economic forces to carry over the risks from the suppliers to the public. The market would remain in its natural state (construction by demand from easily fabricated materials).

The first force is the lettings institution which allowed the separation of ownership from the inhibition and provided consumers with access to real estate with an ongoing flow of payments instead of a one-time payment. Rent allows you to significantly increase the value of real estate and solvency demand, contributes to investment appeal and provides market capitalization that is sufficient to satisfy the demand.

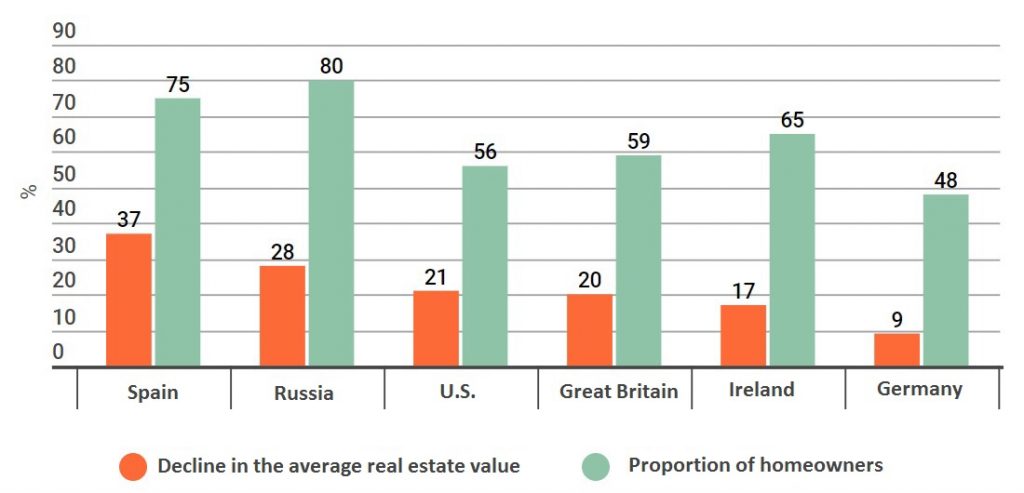

The higher the proportion of the lettings market the less the country is exposed to real estate crises. In Germany, where real estate is owned only by 43% of the population, the financial crisis of 2007 was relatively mild which cannot be said about Spain, where 82% of the state are house owners. For those who are able to combine possession and usage, the mortgage institution plays a similar role. The mortgage value is higher for the investors than the rental value, due to the mortgage cash flow is final and includes ownership transfer.

A SAFE INDICATION FOR AN APPROACHING CRISIS IS THE INCREASE OF CAPITAL AND HOUSING CONSTRUCTION IN GROSS DOMESTIC PRODUCT. ANDREY MOVCHAN, CHAIRMAN OF THE DIRECTOR’S BOARD OF THIRD ROME

Modern builders can afford considerably greater investments in core funds. However risks do not disappear, they accumulate in the banking system and resurface sooner or later. The causes for crisis are not the fluctuations of natural demand and supply but rather tools of balance. Real estate market cycles are longer but crises globalize on their own, covering a whole country or even a group of countries – depending on the geography of the banking system.

The scheme hasn’t changed since 1790’s when Napoleon’s war reduced the crediting opportunities of the British banks, which immediately led into a collapse in the land and real estate markets in the United States as well as in the new capital Washington DC- Up to the crises in 2007-2010. The scheme goes as follows- increase in the proportion of credit against real estate collateral in banking balance sheets; risk mitigation in banking by selling loans to people using a variety of securities; increase in real estate value due to the increase of market’s financial opportunities; decrease of sensitivity against risk in hopes of further growth and finally – triggers which drastically reduce future bank financing opportunities.

Fighting the crisis outcome is simple: the level of available funding gradually recovers but its value decreases due to recession and decline in consumption. If the state is ready to support banks with liquidity and for some time to redeem debts secured by real estate, it accelerates the return of the market to a steady state. Crises are being solved with a temporary reduction in the volume of new construction and reallocation of real estate parts in favour of most solvent owners – given the territorial characteristics do not change for the worst during the crisis.

Several indicators show that the crisis is approaching and the most certain is the increase of capital and housing construction in GDP. In recent history in dawn of the real estate crisis the capital construction increased to 10-12%, housing construction to 5-6% in GDP (exceptions were countries where GDP grew above 6% per year). In Ireland, at the beginning of 2006, the proportion of construction in GDP exceeded 18% while proportion of housing construction reached eight percent. Another important indicator is the lettings volume. Historically it has been proven that if the rental price rate falls below the profitability of medium-term government bonds then the real estate price level is not stable and we can expect a crisis. In the United States, before 2007, the decline was about 1% a year, in Ireland before the crisis it was about 0.5 percent.

The third indicator is a prolonged increase in average wages, significantly outpacing the increase total added value in GDP and real GDP growth. For example, in Ireland, salaries increased by 30% during the first six years of the 21st century meanwhile in the euro area – by an average of ten percent. A continuous growth of real estate value (over five years), outpacing GDP growth of 4% per year or more has always resulted in a real estate crisis in the 20th and 21st century. In the USA and Europe this gap was 4-6 percent in 2000 – 2007.

General trends in developed countries indicate a worsening of real estate crises in the future. In the last 100 years the proportion of mortgages in the bank balance sheets has increased from 30% to 60% as well as the ratio of private debt to GDP has increased on average from 60% to 200%. The share of shadow banks (direct loan, commercial paper, other non-bank funding) in the real estate sector in 2000 exceeded 50 percent. Although it has now dropped to about 40% it is still 1.5 times larger than 15 years ago.

SINCE THE ECONOMY JUST LIKE OIL IS MOVING TOWARDS THE 2004. – 2005 LEVELS THE PRICE PER SQUARE METER MAY TEND TO DO THE SAME.

For the time being there is no reason to talk about real estate crisis approaching Russia. The proportion of capital construction in GDP does not exceed 6-7% and proportion of housing construction is around 3-4%. Even in the period from 2000 to 2007, prices per square meter in Moscow increased less than GDP in dollars (5 times compared to 5,2 times) but since 2007 they have been stagnating although GDP has increased by another 1.5 times. Also wages in Russia grew slower than the GDP did and only slightly faster than the added value. Only rental rates remained stable at around 4% per year while the profitability of Russian medium-term government bonds did not fall below 4%, but currently they are traded at significantly higher yields. This is more indicative to the low demand for rental housing – in Russia 84% of the population own real estate but the labour migration in the country is very low.

However this does not mean that real estate prices could not drop. Decrease in income and GDP, increase in interest rates – all signs are currently indicative of a decline in the value of a square meter in the future. Since the economy just like oil is moving towards the 2004.-2005 levels then the price per square meter may tend to do the same. Only this process will not avalanche and will not lead to mass bankruptcies as it tends to happen in times of crisis.